In the past five years, two systemic shocks have tested the resilience of the modern energy system – a fundamental part of the modern economy: the war in Ukraine and the ongoing conflict in the Middle East. Both events triggered fuel supply shortages and a sharp spike in global energy prices.

These crises, in different ways, have revealed the same structural weakness. Economies that remain heavily dependent on internationally traded fossil fuels are acutely vulnerable to geopolitical disruption, price volatility and supply uncertainty. What begins as a regional conflict or supply shock rapidly becomes an issue affecting global markets, feeding into inflation, interest rates and broader economic growth.

The latest tensions in the Middle East are a further reminder that energy security can no longer be viewed narrowly as a question of maintaining supply. It is increasingly about reducing exposure to external fuel-price driven shocks altogether. This is a key structural tailwind for the global energy transition.

Supply-side shocks

Oil and gas markets remain highly sensitive to geopolitical developments, with even relatively small changes in supply expectations capable of moving prices sharply. Those price movements then cascade through economies via current and medium-term wholesale gas and electricity prices (see below example based on UK data), as well as through transport costs, industrial production and, ultimately, consumer inflation.

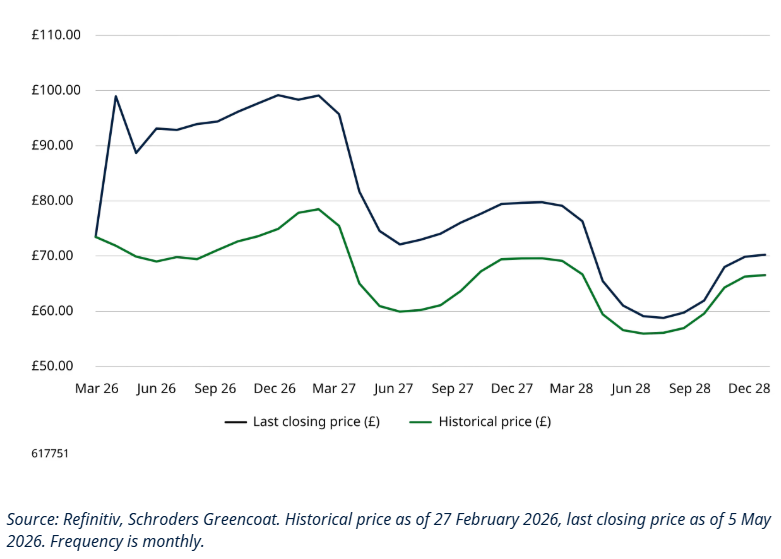

Wholesale electricity prices have surged

UK future wholesale electricity prices (£/MWh), March 2026-December 2028

For policymakers, this creates a familiar but increasingly difficult dilemma: inflationary pressure driven by supply-side issues and input costs is notoriously hard to contain through the traditional mechanism of interest rate rises, which are designed to curb demand. Tightening policy too aggressively risks undermining growth, while failing to contain inflation raises the prospect of stagflation.

Demand-side shifts

If energy markets are currently a key focus in economics and monetary policy, then demand dynamics – specifically rising demand for power – are similarly altering the equation.

In the digital age, electricity is assuming an economic role comparable to the one oil played during the industrial age. The artificial intelligence revolution, data centre boom, and ongoing electrification and digitalisation of sectors across the economy is driving up demand for electricity – in some places for the first time in more than a decade.

Given the scale of the growth expected over the coming years (see chart), this in turn transforms electricity from a background utility into a core determinant of economic competitiveness.

Renewables capacity to quadruple to meet growing energy demand

Data centres provide perhaps the clearest illustration of this shift. As computational intensity rises, so too does electricity demand. While affordable power is an important consideration in the build out of data centre assets, the most critical piece of the puzzle is being able to access grids and reliable electricity. This is increasingly becoming a prerequisite for growth in the sectors driving productivity and innovation, and so to broader economic outcomes.

Energy security and economic resilience

Taken together, this changes the nature of what energy security means. Historically, concerns around energy supply were concentrated in heavy industry, manufacturing and transport. Today, energy risk is becoming embedded in the broader economy.

In that context, the reliability and cost of electricity matter more than ever. The recent short-term spike in energy prices has caused an economic shockwave; longer term, sustained volatility in power prices feeds directly into corporate margins, investment decisions and long-term competitiveness. Economies capable of delivering stable and affordable electricity are likely to enjoy a structural advantage.

The transition towards electrification therefore represents more than a decarbonisation strategy. Increasingly, it is an economic resilience strategy – both in terms of reducing reliance on imported fossil fuels and reducing exposure to heightened global energy price volatility.

Renewable energy technologies possess a distinctive characteristic that differentiates them from fossil fuel systems: once built, they operate without ongoing fuel costs. While renewable infrastructure can be capital-intensive upfront, operating expenses tend to be comparatively low and stable because generation is not tied to volatile internationally traded commodities.

Energy transition: Divergence in global approaches

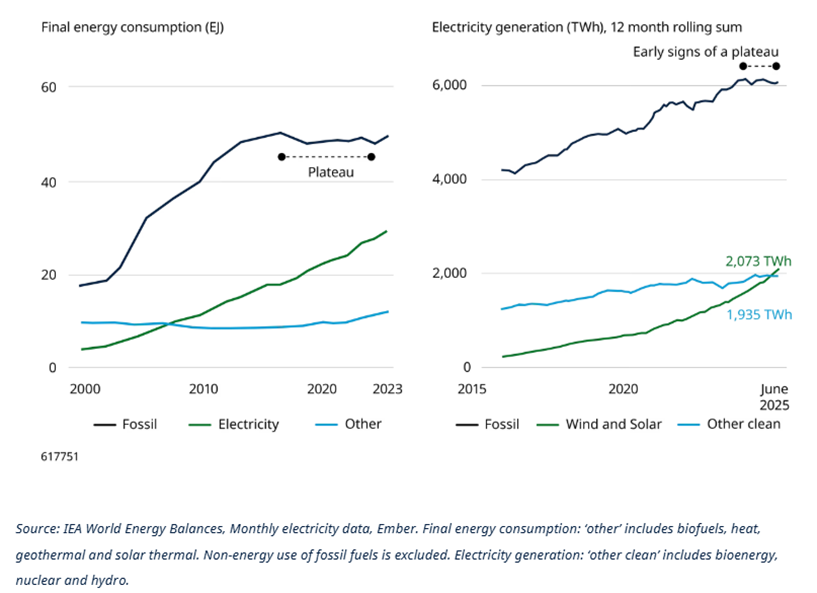

The implications are visible in the differing approaches major economies are taking towards energy policy. China has pursued perhaps the most coordinated strategy, combining rapid renewable deployment with widespread electrification of transport and heating. The effect has been to reduce exposure to imported fuels and global commodity-price volatility.

The shift is now visible in the data. Clean generation met the bulk of China’s incremental electricity demand in 2024, and in early 2025 it exceeded it, reducing dependence on traditional fossil fuel generation. The broader aim is that more energy demand can be met through domestically generated electricity, decoupling the economy from swings in fuel markets.

China fossil fuel consumption is plateauing as clean energy generation rises

The US, by contrast, is pursuing a less straightforward path. Renewable investment continues to grow rapidly, but alongside this Washington has maintained strong support for domestic oil and gas production; the US is the largest individual oil producing nation on earth. That strategy offers short-term flexibility and supports domestic energy supply – and has boosted short-term export revenues. Yet despite this, we continue to see significant activity in the US around renewable energy, both given the cost advantages that renewables have in windy and sunny areas in the US, but also the role that renewables can play as the technology with the fastest route to market in a period where expected electricity demand is expanding rapidly.

Europe offers another instructive case study. The energy crisis triggered by Russia’s invasion of Ukraine in 2022 forced a rapid reassessment of the continent’s dependence on imported natural gas. The resulting policy response accelerated investment in renewables, energy diversification and electrification.

Spain presents a clear illustration of how diversification is beginning to feed through into pricing. While it is true that Spain’s renewables market has not always delivered a smooth experience for investors, it does show that sustained investment in renewables – coupled with favourable conditions for renewables generation in the form of disproportionately sunny and windy weather conditions – has reduced the role of natural gas in setting electricity prices.

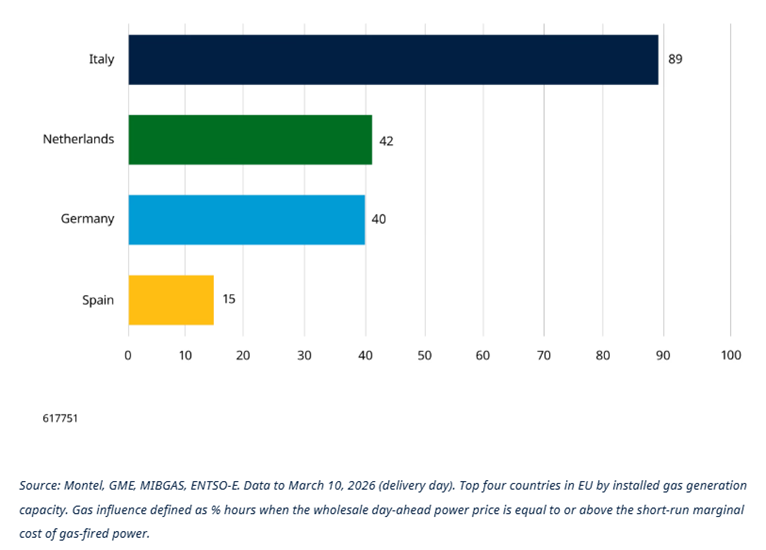

In 2026 so far, market prices for gas have driven electricity pricing during roughly 15% of hours in Spain, defined as hours each day when wholesale power prices are at or above the short-term marginal cost of gas-fired power, compared with close to 90% in Italy. In the UK this figure has fallen from 85% in 2021 to around 60% today, according to figures from the National Energy System Operator (NESO).

Gas influence on power prices varies by EU country

Across Europe, the picture points in a similar direction. Renewables accounted for more than 47% of EU electricity generation in 2025, suggesting that resilience is increasingly being built through a shift in the structure of supply, rather than through short-term policy responses.

Energy transition and the evolving risk map

None of this implies that the energy transition removes system or geopolitical risk entirely. Rather, it changes where that risk resides.

Historically, energy security centred on access to oil and gas reserves concentrated in a relatively small number of regions. The transition towards electrification shifts attention upstream towards manufacturing, technology supply chains and critical minerals. This introduces a new set of strategic sensitivities.

Critical minerals such as lithium, copper and rare earth elements are becoming increasingly important to the production of batteries, power electronics and renewable infrastructure. At the same time, manufacturing capacity for many clean energy technologies remains heavily concentrated geographically. In particular, the West’s relationship with China, a key source of key minerals and the leader in technology manufacturing, could come into sharper focus.

The resulting question is whether economies are simply replacing one dependency with another. There are important distinctions, however. Fossil fuel reserves are largely (and irrevocably) determined by geography. Renewable supply chains, manufacturing capacity and grid infrastructure can be shaped more directly through industrial strategy, investment and policy. And renewable supply chains are primarily relevant to construction of new capacity; once built the assets operate for decades with little ongoing reliance on their original providers.

Short-term policy attention and investment is also required to upgrade aging grid infrastructure, which is ill-equipped to cope with the more intermittent nature of renewable energy. Permitting delays and transmission bottlenecks are other emerging critical constraints in many markets.

These are obvious ‘pinch points’ that will require investment to unlock the full potential of the transition. Building renewable generation capacity alone is not enough; economies must also invest in the networks and storage systems required to distribute electricity reliably.

What does this mean for investors?

What does all of this mean in practice – and why should investors care?

In the short term, many energy transition infrastructure assets with merchant price exposure have benefited from rising power prices without the corresponding increase in operating costs faced by fuel-dependent generation assets. We have seen this dynamic play out across our own portfolios. This has come at a particularly valuable time, with rate increases and inflation putting other predictable cash flow streams under pressure.

More critically and longer term, the fact that economies have been rocked by a second energy price driven shock in five years is creating more structural tailwinds and a refocusing of government attention towards supporting and investing in energy transition infrastructure opportunities.

In many regions there were already ambitious plans in place that would require substantial private capital to fund. The IEA has estimated that $4.5 trillion needs to be invested in the energy transition per year from 2030 – and energy transition has already been by far the most active segment within infrastructure investment over a number of years. This promotes a broad and ever deepening opportunity set for investors.

Crucially, the opportunity is widening beyond traditional renewables such as wind and solar. Reducing dependence on oil and gas, and maximising the potential of clean energy generation, will also require development of electrified heating; alternative clean fuels such as green hydrogen and biomethane; battery storage to manage intermittent renewable energy load; and investment to upgrade aging grid infrastructure.

Beyond there simply being more opportunities, energy transition infrastructure offers significant potential portfolio diversification, resilience and performance benefits. This is an area that offers exposure to a highly differentiated set of risk exposures, access to both reliable and inflation-linked cashflows as well as capital growth potential. It has delivered outcomes that are uncorrelated to other asset classes, including broader diversified private infrastructure – including significant outperformance during the last fuel price-driven downturn in 2022.

It is also an area that has grown in complexity and nuance, and which is now very multi-faceted in terms of the investible opportunities and the understanding required to invest effectively. For this reason, the role of specialist investors able to navigate different systems, technologies, regulatory regimes and grid operators has become more important than ever.

A new definition of resilience

Developing more domestically-oriented clean energy sources, alongside technologies that reduce the reliance of hard-to-abate sectors on oil and gas, should help to insulate economies from energy price-driven economic shocks. It should also provide support for and stabilise power prices over time, improving energy affordability – another key priority for governments.

These all speak to energy and economic resilience. For investors, energy transition infrastructure is set to benefit from tailwinds that will broaden an already wide funnel of opportunities, increasing the potential sources of resilience for their own portfolios.

More broadly, the energy transition represents a major reallocation of capital across generation, storage, transmission and electrification. Recent crises have reinforced the idea that economic resilience cannot rest solely on central banks or fiscal intervention – and it cannot be solely a reactive impulse after-shocks emerge. Increasingly, it depends on how energy systems themselves are structured.