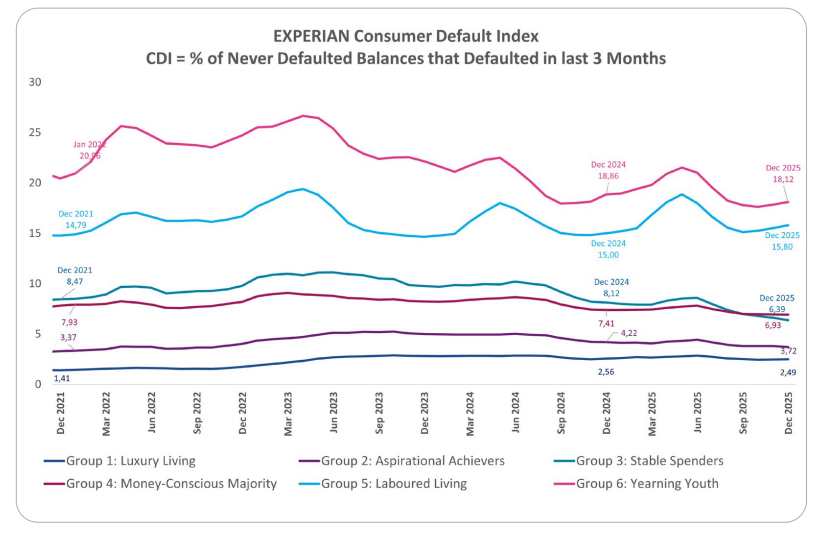

South African consumer credit trends show a significant shift in repayment behaviour, with homeowners prioritising mortgage payments, leading to a 20% year-on-year improvement in home loan defaults, according to the latest Experian Consumer Default Index (CDIx) for Q4 of 2025. However, the report reveals a complex picture, with underlying data indicating that many consumers are turning to unsecured credit to manage ongoing economic pressures.

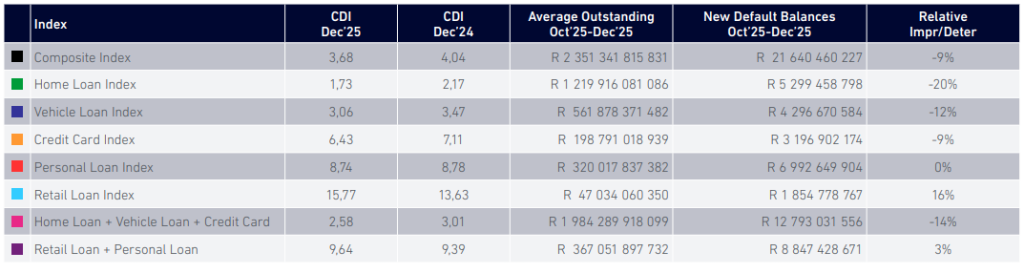

The Experian CDIx tracks how often South Africans default on their debts for the first time. It measures the sum of first-time defaulted balances as a percentage of the total outstanding balances across five key credit products: home loans, vehicle loans, personal loans, credit cards, and retail loans.

The national default rate, or Composite CDI, improved from 4.04% to 3.68% over the past year. This 9% relative improvement suggests that, while many households still find it challenging to honour their commitments, the overall situation is slowly improving.

Home Loans Pave the Way for Recovery

The key finding for this quarter is the significant improvement in the Home Loan CDI, which fell from 2.17% to 1.73% year-on-year. This is primarily driven by mid-to-high affluence consumers, who hold most of the mortgage debt, beginning to stabilise their financial positions.

“The sustained improvement in home loan performance is a positive recovery indicator, as mortgages represent the largest portion of consumer debt,” said Jaco van Jaarsveldt, Chief of Strategy and Innovation at Experian Africa. “This trend, coupled with a 12% year-on-year improvement in vehicle loan defaults, suggests that consumers are successfully prioritising their secured debt repayments, even in an environment where the improvement can partially be attributed to the lack of supply which statistically translates into improved default rates.”

Provincially, all nine provinces saw an improvement in their Home Loan CDI. The Western Cape continues to have the lowest default rate, while Gauteng recorded the most substantial absolute improvement.

Affluent Segments Under Pressure

Despite the positive headline figures, the data reveals a more complex picture beneath the surface. While defaults on large, secured loans are decreasing, affluent consumers, traditionally seen as low-risk, are showing clear signs of financial strain elsewhere.

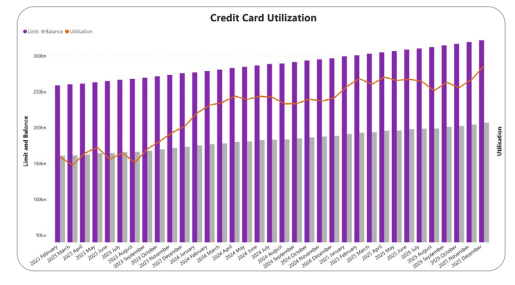

Credit card utilisation has been on a steady upward trajectory, with 79% of total exposure concentrated among high-affluence consumers (FAS Groups 1 & 2). This indicates an increasing reliance on revolving credit to manage the rising cost of living. Furthermore, these same affluent segments have seen their default rates for unsecured products like personal loans and credit cards deteriorate over the past year.

“The fact that affluent consumers are keeping up with mortgages but falling behind on unsecured credit and using credit cards more to get by is a red flag,” notes van Jaarsveldt. “It tells us that even high-income households are feeling the pressure. They are being courted by multiple lenders, leading to expanding credit exposures that are stretching their affordability to its limits.”

Navigating a Complex Credit Landscape

The Q4 2025 data reveals a mixed credit market where headline improvements mask deeper complexities. On one hand, the significant recovery in home loan performance shows that consumers are fiercely protecting their primary assets. On the other hand, the growing reliance on credit cards and signs of strain in unsecured loans, particularly among affluent segments, highlight a persistent battle with day-to-day affordability. This points not to a simple recovery, but to the emergence of a new consumer reality defined by careful financial trade-offs.

“This environment means a one-size-fits-all approach to credit is no longer viable. The market is fragmented, and even consumers who appear financially healthy are navigating hidden pressures. For lenders, this highlights the need for deeper, data-driven insights to understand the true financial position of their customers. By doing so, we can power new opportunities, foster responsible lending, and support financial health for all South Africans,” concludes van Jaarsveldt.

Experian remains committed to empowering consumers with free tools like Up, a web-based app, which provides credit information and education to help them navigate their financial journeys with confidence.