The energy shock triggered by the closure of the Strait of Hormuz at the end of February 2026 is reverberating through the world economy, with the full extent of its impact – including likely complex knock-on effects – far from clear. This is the second major energy shock of the 2020s, with many economies still adjusting to the first triggered in 2022 by Russia’s invasion of Ukraine.

Looking further back to comparable shocks of the 1970s highlights the potentially profound consequences that could stretch decades ahead.

As nations and trade blocs rush to fortify their energy supplies, they embark on new policy directions with implications touching every industry and asset class. For investors this brings new risks, as well as opportunities. It may, for example, throw open policy revisions relating to hydrocarbon projects. But it could also reinforce the case for a “decarbonisation dividend”, with homegrown, low‑carbon energy reducing import dependency. In this paper we take an investor’s view of the current crisis, seeking to identify likely scenarios to emerge from the disruption and the opportunities these might present.

The energy shock of 2026: who is most exposed – and why it matters

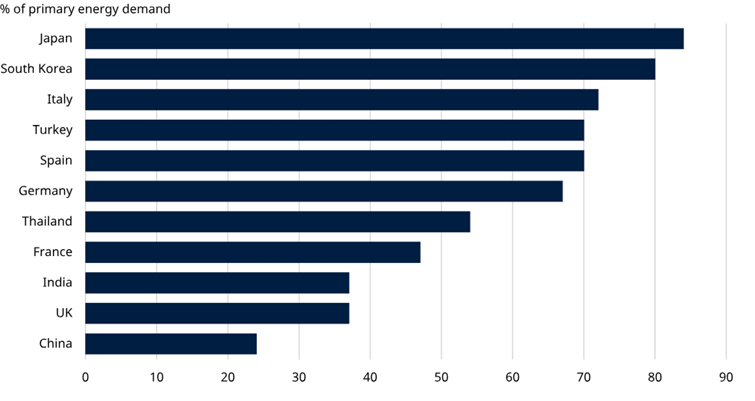

Asian economies are likely to be hit hardest by the disruption. They import more than 80% of the oil and gas shipments that pass through the Strait of Hormuz, leaving them highly vulnerable to supply interruptions and price spikes. Europe’s direct exposure is smaller. It imports only around 5% of its crude oil and 13% of its LNG via the Strait, but it is far from insulated. Energy is priced in global markets, and a scramble for LNG cargoes – with Europe and Asia competing head-to-head – could keep prices elevated for longer.

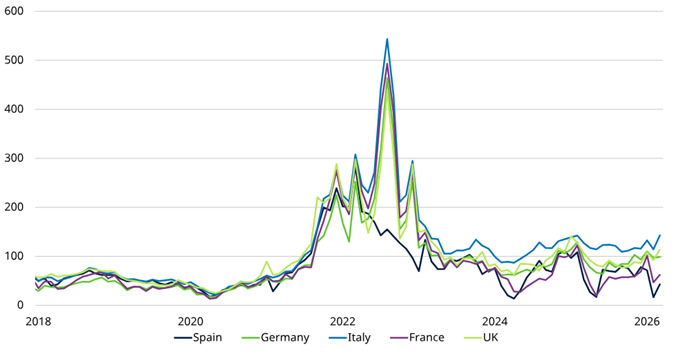

Vulnerability is greatest where import dependence is highest. In Asia, Japan appears most exposed to rising fossil fuel prices, importing 84% of its energy demand, followed closely by South Korea at around 80%. In Europe, Italy, Spain and Germany import more than two-thirds of their energy. With trade routes disrupted and energy costs rising, these economies face a classic stagflation threat: weaker growth alongside renewed inflationary pressure.

A shock that accelerates structural change

Energy shocks rarely end with a simple reversion in prices. More often, they force a rethink of energy strategy, as governments and companies urgently reassess resilience, diversify supply, and accelerate investment in energy systems that are less volatile and less exposed to geopolitical disruption.

We have seen this pattern before.

History rhymes: the oil shocks of the 1970s

The oil embargo of 1973 and the subsequent supply shock in 1979 exposed a profound vulnerability at the heart of industrial economies: overwhelming dependence on fossil fuels imported from geopolitically unstable regions. The result was not merely a temporary increase in fuel prices, but a structural shift in energy policy across many oil-importing countries.

In the early 1970s, fossil fuel consumption was surging and the industry was booming – until supply was abruptly curtailed. Governments were forced into rapid measures to restrain consumption, and households and businesses had to change behaviour. The lesson was stark: when energy security is compromised, policy responses can be swift and far-reaching.

Different responses; different outcomes

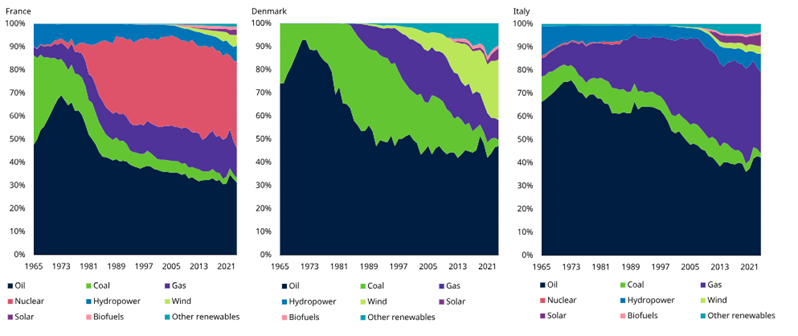

France and Denmark provide clear examples of how swings in fossil fuel prices can catalyse long-term energy transitions, with energy security becoming a national priority and governments pivoting away from imports towards domestic supply.

France responded decisively, launching the Messmer Plan directly in reaction to the oil shock. The result was the fastest large-scale nuclear buildout in modern history, reshaping the country’s power system for decades. Denmark pursued a different route. It intensified exploration in the Danish sector of the North Sea, becoming self-sufficient in natural gas by 1984 and in oil by 1993. At the same time, Denmark became an early pioneer in commercial wind power during the 1970s. This helped to seed an industry that later became globally significant, with Danish manufacturers and component suppliers playing a central role in wind turbine supply chains.

Italy illustrates a contrasting approach. Rather than materially reducing dependence on imported fossil fuels, it remained heavily reliant on energy imports, with policy focused more on diversification: shifting from oil towards gas imports, mainly from Northern Africa and Russia. This period saw a wider Western European pivot to Russian gas, with the construction of pipelines linking the Soviet Union to Western Europe laying the foundation for dependence that grew significantly in subsequent decades. By 2021, Russia supplied roughly 45% of total EU gas imports (including pipeline gas and LNG). This reliance became a critical energy-security issue after Russia’s 2022 invasion of Ukraine, prompting a sharp reduction, down to 19% by 2024. Europe was forced once again to diversify its energy supply, with Russian gas partially replaced by US LNG.

Energy consumption by source

The decarbonisation dividend: security as well as sustainability

The invasion of Ukraine highlighted energy security as an additional driver of the transition away from fossil fuels. Renewable power is not only a pathway to lower emissions, but also limits import dependence.

The surge in gas prices following the invasion forced another rethink in energy strategy, with the EU committing to phase out its dependency on Russian fossil fuels, diversify gas supplies, and accelerate the rollout of renewables.

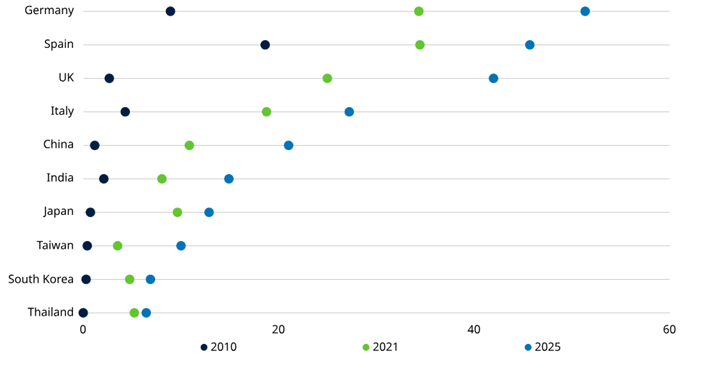

Renewable share of electricity generation (%)

In Europe, momentum has been tangible. In 2025, wind and solar generated more electricity in the EU than fossil fuels for the first time, limiting Europe’s exposure to the type of external shock it faces now. Asian countries were also affected by the 2022 energy shock through rising energy prices. As shown in the chart above, this resulted in a higher renewable share in electricity production across Asian economies as the relative cost advantage of renewables versus oil and gas became clear.

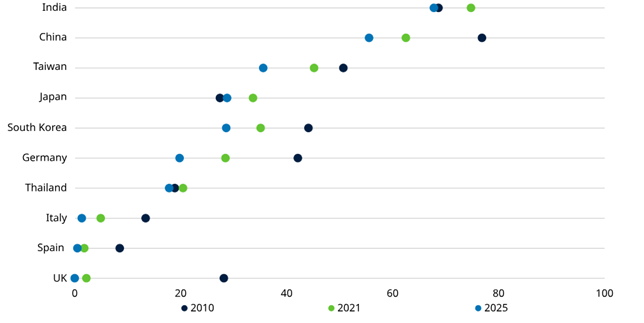

Did countries move back to coal as a result of the Russia-Ukraine conflict?

Some countries pivoted back to domestic coal, but the switch was short-lived and primarily an emergency measure. Coal’s share in electricity continued its longer-term downward trend. Even in major domestic coal-producing countries such as India and China, coal’s share has diminished over the past decade.

Part of the explanation is policy. Carbon-pricing mechanisms make coal less attractive, given it is the most carbon-intensive energy source. Analysis from Bruegel – a European think tank – suggests that after the announcement of the EU’s Carbon Border Adjustment Mechanism (CBAM) in 2019, countries with higher EU trade exposure in CBAM-covered goods were more likely to announce their own carbon-pricing mechanisms. Evidence also indicates that several countries are aligning carbon pricing with sectors covered by CBAM. China, for example, has added steel, cement, and aluminium to its national emission trading scheme (ETS). With CBAM entering into force in January 2026, a durable switch back towards coal among major exporters to the EU looks less likely.

Coal’s share of electricity generation (%)

What are likely impacts on future national energy strategies?

Despite the measures described above in relation to previous oil shocks, the closure of the Strait of Hormuz suggests that lessons around energy security have not been fully absorbed. Dependence on imported fossil fuels still leaves economies vulnerable, particularly through LNG.

In the near term, governments may build larger stockpiles of oil and gas as a buffer while longer‑term solutions are developed. Expanding storage capacity is typically faster than deploying new generation infrastructure, particularly given current grid bottlenecks and limited grid capacity.

Investor view: how the crisis highlights an emergent energy cycle

Mark Lacey, Head of Thematic Equities and Portfolio Manager, Global Resource Equities

There were signs that available oil supplies were likely to fall short even before the current conflict in the Middle East threatened unprecedented disruption.

The effective closure of the Strait of Hormuz is a major supply shock, landing in markets that were already tightening. In that sense, the conflict is bringing forward a repricing rather than creating a wholly new dynamic: oil balances were becoming less comfortable, with gas markets expected to tighten over the next three to four years.

This shock also exposes the consequences of a decade of underinvestment. The energy sector’s weight in global equity indices has fallen from around 14% at prior peaks to roughly 3% in early 2026, as capital discipline and shareholder returns took precedence over new supply. Reserve lives have shortened (from 14–15 years in the early 2000s to ~7–10 years for many producers), and beyond 2026 there are fewer confirmed projects to add material production. Meanwhile, the rapid “swing supply” once provided by US shale appears less responsive and more capital-intensive.

Demand, however, is shifting rather than fading. US Electricity demand is expected to grow around 2–3% per year, driven by electrification and data-centres supporting AI. In some cases the latter add to gas demand via on-site turbines.

A more durable pricing backdrop can support energy cash flows and equities; and as governments prioritise energy security, the opportunity set broadens to grids, storage, renewables and enabling technologies.

Why renewables matter for security (and cost)

The Iran conflict brings renewables back into focus as a strategic means of securing power independence. Solar and wind technology do not require fossil fuel inputs, so their generation costs are less exposed to swings in global energy markets.

In European power markets, the most expensive generator operating to meet demand – typically gas – often sets the hourly wholesale electricity price. As electricity production from lower-cost technologies like wind and solar expands, it displaces gas and coal more frequently, meaning fossil power sets the price less often.

Spain provides a clear example. Analysis from Ember, the global energy think tank, finds that strong solar and wind growth has helped Spanish electricity prices start to decouple from gas prices. In the first half of 2019, Spain’s power prices reflected the cost of fossil generation in 75% of hours; by the same period in 2025, this fell to 19%. Even with the sharp rise in gas prices following Iran’s conflict, Spain’s electricity remains among the cheapest across Europe and the UK.

Wholesale electricity prices

Investor view: are equity markets correctly pricing the long-term impact?

Simon Webber, Head of Global Equities

There is already clear evidence that higher and more volatile fossil fuel prices are translating into stronger demand across wind, solar and grid‑scale energy storage (see Renewable infrastructure becomes more attractive, below). Order books in these segments are beginning to re‑accelerate as utilities and governments bring forward investment to lock in lower‑cost, domestically produced power. Yet equity markets remain sceptical. Share prices and valuations across much of the renewables value chain continue to imply that this is a short‑lived cyclical upswing, rather than the start of a more durable period of higher growth driven by energy security considerations. This disconnect leaves select parts of the sector pricing in little recognition of improving fundamentals or increased visibility on future demand.

Outside the US, high and volatile oil prices are also re‑accelerating the transition to electric vehicles. This favours manufacturers and suppliers that stayed the course on EV investment through the recent cyclical slowdown, and exposes those that delayed or retrenched. Market share shifts are now more likely to be structural rather than cyclical.

At the same time, higher fossil fuel prices and stronger demand for industrial metals are driving renewed investment in upstream energy and mining capacity. The primary beneficiaries extend beyond commodity producers themselves to industrial companies supplying mining equipment, energy production services and electrical infrastructure. Firms exposed to power grids, electrification and energy reliability sit at the intersection of security‑driven policy support and rising capital expenditure to meet rising electricity consumption.

By contrast, the environment is far less forgiving for consumer‑exposed sectors. Energy and commodity inflation is feeding into another round of input cost pressure at a point where consumers are already resistant after the post‑pandemic inflation shock. Margin erosion will likely be widespread, with only those companies able to demonstrate genuine pricing power and brand strength likely to emerge unscathed.

The banking sector also faces a less benign outlook. After benefiting from higher interest margins and low credit costs, cracks are beginning to emerge. Some lenders with exposure to agriculture, logistics and lower‑income consumers are already signalling higher non‑performing loan expectations. If oil prices remain close to $100 per barrel, energy‑driven inflation risks translating directly into broader credit stress.

Investor view: renewable energy infrastructure becomes more attractive

Duncan Hale, Portfolio Manager, Schroders Greencoat

There is likely to be increased long-term focus on expanding energy security and affordability through domestic, low-carbon sources – including the continued build-out across many regions of core renewables (wind, solar) and emerging technologies and fuels (green hydrogen, district heating networks, and transmission networks).

These dynamics also support the risk-return case for energy transition infrastructure. Gas prices, in particular, have a pronounced knock-on effect on power prices, meaning Europe and the UK are especially exposed. For renewables assets with merchant price exposure, this can provide a boost to short-term returns.

We have seen this dynamic play out in Schroders Greencoat’s portfolios, where periods of rising broader power prices have had a direct positive impact. The last time a geopolitical conflict meaningfully impacted gas and power prices — at the start of the Russia-Ukraine conflict in 2022 – strong calendar-year returns followed. In fact, across the wider market, 2022 saw equities and bonds fall in tandem and most private market asset classes, including diversified infrastructure equity strategies, posting single digit positive returns. Energy transition infrastructure returned more than 22%.*

This episode also highlights the diversification benefits of an energy transition allocation within a broader portfolio. Power prices, inflation, and resource availability are the core drivers of returns in this sector, and these factors tend to have low, or even negative, correlation with many traditional asset classes. We could expect similar outcomes from the current shock: higher power prices and inflation are expected to have a positive impact on energy transition infrastructure assets, even as they weigh on broader equity and credit markets.

Do renewable energy options bring their own supply risks?

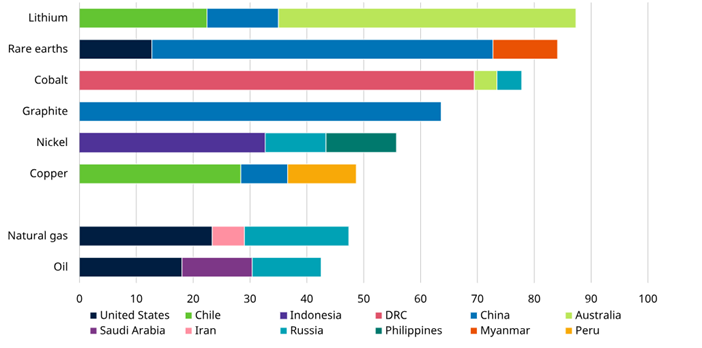

Clean energy technologies, including wind turbines, solar panels and electric vehicles, are much more mineral-intensive than fossil fuel energy. For example, an offshore wind plant requires around 13 times more mineral resources than a gas plant. As a result, the transition will drive a substantial increase in demand for minerals and metals. The security challenge is that the minerals needed to transition to clean technologies are concentrated in a small number of countries. Supply chains for transition materials are more geographically concentrated than those for oil or natural gas.

The chart below shows the share of top three producing countries in extraction of key minerals and fossil fuels, highlighting how production of lithium, cobalt, and rare earth elements is controlled by a handful of suppliers.

The concentration is particularly striking in cobalt and rare earths. The Democratic Republic of the Congo produces around 70% of global cobalt supply – a key metal for electric vehicle batteries – while China accounts for 60% of global production of rare earth elements. China also dominates graphite production, another critical battery input. Meanwhile, tensions between Europe and Russia could further complicate the transition, as Russia is an important producer of nickel and cobalt.

Where key minerals are mined

That said, solar and wind provide a distinct resilience advantage versus fossil fuels: their primary energy inputs are not cargoes that can be delayed, rerouted, or blocked at chokepoints like the Strait of Hormuz.

While restrictions on critical minerals can constrain future deployment, they do not impair the operation of installed renewable capacity. Moreover, because generation costs are not linked to fossil fuel inputs, existing renewable output can remain economically and operationally stable even during periods of sharp oil and gas price volatility.

Implications: a reshaped commodities cycle – and winners in the transition

As analysed in a recent paper the energy transition is likely to have a major impact on the global commodities market. Scaling clean power requires large volumes of industrial metals, supporting long-run demand and potentially creating a “twin-speed” super‑cycle: fossil fuel prices trend lower over time, while industrial metal prices rise.

For emerging markets (EM), the investor implications are significant and uneven. Countries that rely heavily on fossil fuel export revenues may face persistent external and fiscal pressures as demand and prices weaken. They will have to adapt their economies and public finances to the new, low-carbon economy, or face economic and market stress. This will be a major issue for EM that have little in the way of savings from past exports. A permanent improvement in the balance of payments of EM that are net importers of fossil fuels should be supportive of currencies and structurally lower interest rates in the long term. But the biggest opportunities for investors will probably be found in those EM that export much sought-after commodities in the new world, which should boost returns across the board.

Written by Irene Lauro, Senior Economist – Europe and Climate at Schroders