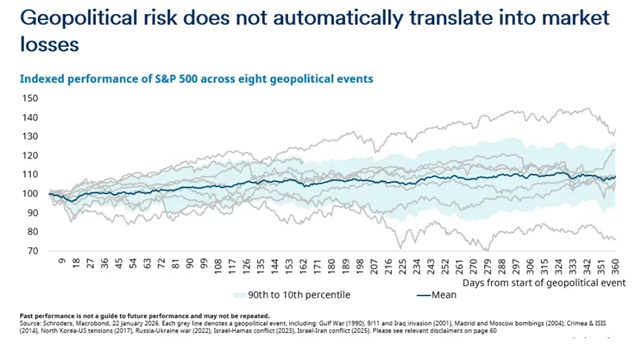

Despite the recent rally, recent heightened geopolitical risk and a soaring oil price have broadly caused global equities to sell off.

That said, historically, geopolitical risk does not automatically translate into market losses.

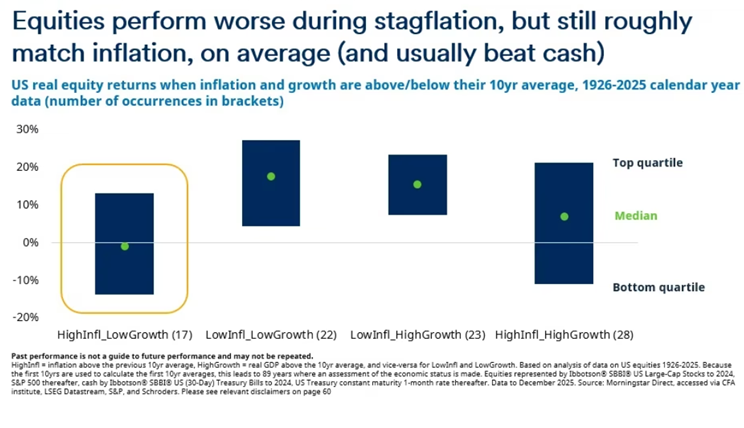

Rising energy prices increase the risk of stagflation (high inflation/low growth)

Over the past 100 years, stagflation has been a challenging environment for equities. But, while the market noise can be difficult to stomach, equity performance during stagflationary periods have roughly matched inflation on average and usually beaten cash.

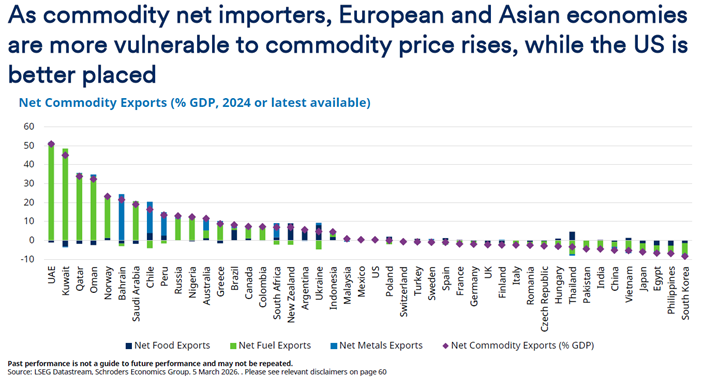

Commodity importers will feel the squeeze

On an economic basis, as commodity net importers, European, Asian and some emerging market economies (like South Africa) are more vulnerable to commodity price rises. The US, however is more insulated in this respect.

Sectoral and regional insights

On a sectoral basis, the UK equity market is notably overweight defensive sectors such as energy, consumer staples, healthcare and utilities, which have historically performed relatively well during periods of sharp oil price increases. By contrast, Japan and emerging markets have more challenging sector exposures, while the US and Europe also show vulnerabilities during energy price shocks.

Market dispersion has increased meaningfully, with a rising proportion of countries and companies outperforming the broader market. This reflects a shift away from highly concentrated leadership, particularly in developed markets. Emerging market equities are an exception, however, where performance remains heavily concentrated in a small number of mega‑cap stocks.

Value equities stand out as having a low correlation with AI‑related stocks and have delivered materially better outcomes during periods when AI stocks have sold off. Importantly, many passive approaches to value investing still retain significant exposure to large technology names, limiting their effectiveness as a hedge against AI‑related risk.

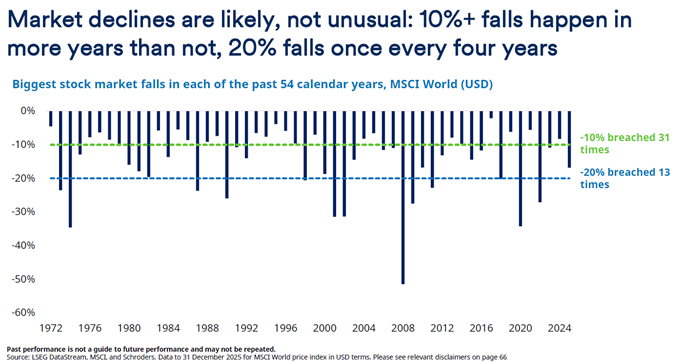

Long‑term lessons from equity market history

Historical analysis shows us that market declines of more than 10% occur in more years than not, while 20% drawdowns have historically happened roughly once every four years. On average, markets experience an intra‑year fall of around 15% alongside a rise of approximately 23%.

Although periods of heightened volatility can feel unsettling, exiting markets during these episodes has historically been damaging to long‑term wealth outcomes. Equity investing can be particularly uncomfortable in the short term, but equities have proven less risky than cash when assessed by their ability to deliver inflation‑beating returns over time. Ultimately, there is always a reason for concern, but over the long run, equities have outperformed bonds, which in turn have outperformed cash.

Written by Duncan Lamont, CFA, Head of Strategic Research at Schroders